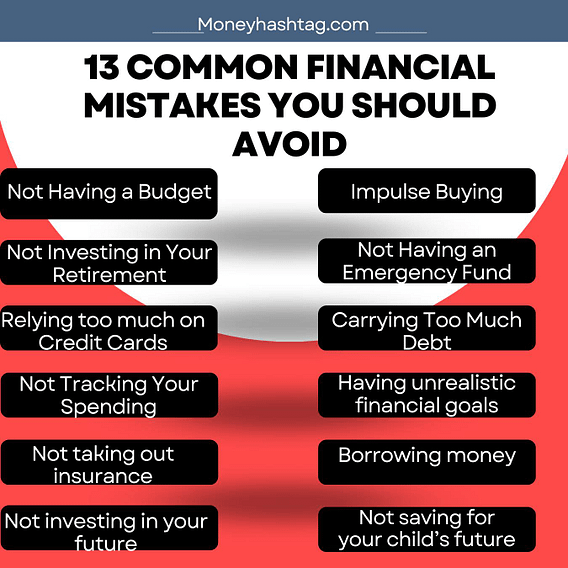

13 Common Financial Mistakes You Should Avoid

Becoming financially free is a journey that requires discipline, hard work, and proper planning. In a world where money is continuously flowing, it is important to be aware of the common financial mistakes that can both cost us dearly and set us up for long-term struggles. Everyone wants to be secure and financially sound.

Do you worry about making mistakes with your finances? Financial mistakes can be costly, but they are also avoidable. In this article, we will go over some common financial mistakes and how you can avoid them so that you can get the most out of your money.

Common Financial Mistakes

There are a lot of financial mistakes that people make daily. Some of these mistakes are so common that they almost seem like they are unavoidable. Luckily, this is not the case. If you are aware of the most common financial mistakes people make, you can avoid them altogether.

Not Having a Budget

One of the most common financial mistakes is not having a budget. A budget is a plan that tells you how much money you have to spend and where you have to spend it. It allows you to track your spending and make sure you are staying on track with your financial goals. Without a budget, it is easy to overspend and get into debt.

If you have not started it yet, you better not waste your time and get into creating a budget for yourself.

Impulse Buying

Impulse buying is a common financial mistake that can lead to serious debt problems. It is important to be aware of your spending triggers and learn to control your impulses. If you are thinking about making an impulse purchase, ask yourself if you really need the item.

If it is something you can live without, then it is probably not worth your money. It is also important to consider whether you can afford the item. If it is going to put a strain on your finances, then it is probably not worth it.

If you do decide to make an impulse purchase, be sure to do your research and compare prices before you buy. This way, you can be sure you are getting the best deal possible.

Not Investing in Your Retirement

One of the most common financial mistakes people make is not investing in their retirement. This can be a costly mistake that can leave you without enough money to live comfortably in retirement. Retirement may seem like a long way off, but the sooner you start saving, the better.

There are a few different ways you can go about investing in your retirement. The most common way is to invest in a 401k or IRA. These are retirement accounts that are offered through your employer or bank. They typically offer tax breaks and other benefits that make them a great way to save for retirement.

Every country has their different retirement programs. Whatever method you choose to invest in your retirement, it is important to start as early as possible. The more money you have saved for retirement, the more comfortable your retirement will be.

Not Having an Emergency Fund

When it comes to financial security, one of the most important things you can do is to make sure you have an emergency fund. This is a savings account that you can use in case of unexpected expenses, like a job loss or a medical emergency. Not having an emergency fund can leave you vulnerable to debt if something unexpected happens.

Without an emergency fund, you may have to put these expenses on a credit card, which can lead to debt. There are a few different schools of thought on how much you should have in your emergency fund.

Some people recommend saving enough to cover three to six months of living expenses, while others say you should save enough to cover one year’s worth of expenses.

It is important to start saving for your emergency fund as soon as possible. Begin with $50-$100 per month and increase the amount as you can. That way, if something does happen, you will have the financial resources you need to get through it.

Relying too much on Credit Cards

If you find yourself relying too heavily on credit cards, it is important to take a step back and reassess your finances. Credit cards can be a helpful tool when used responsibly, but they can also lead to debt problems if you are not careful.

If you carry a balance on your credit card from month to month, you will end up paying interest on that balance. Over time, the interest charges can add up, making it difficult to pay off your debt.

If you miss a payment on your credit card, you will be charged a late fee. Missed payments can also damage your credit score, making it harder to get approved for loans or new lines of credit in the future.

It can be easy to overspend when you’re using a credit card, especially if you don’t have the cash on hand to pay off your balance right away.

When you use your credit card to regularly make impulse purchases or withdraw cash advances, you may find yourself in a difficult financial situation.

Thus, credit cards usage should be lessened to avoid financial ruins.

Carrying Too Much Debt

Debt can be a good thing or a bad thing, depending on how it is used. Good debt is used to finance investments that will grow in value over time, such as a home or an education.

Bad debt is used to finance consumable items that will quickly lose value, such as a car or a vacation.

But when your bad debt starts to outweigh your good debt, it is a sign that you are in financial trouble. Not only does it put a strain on your finances, but it can also lead to other problems down the road.

Carrying too much debt can be a major burden financially. It can lead to financial stress and even ruin your credit score.

Not Tracking Your Spending

If you are not keeping track of your spending, you could be making some serious financial mistakes. It is important to know where your money is going so you can make informed decisions about your finances. There are a number of ways to track your spending, including using a budget, tracking your receipts, and using personal finance software.

Budgeting is one of the best ways to track your spending and make sure you are staying on track with your finances. When you are not tracking your spending, it is easy to overspend on items that you don’t really need.

There are a number of different budgeting methods you can use, including the envelope system, the 50/30/20 rule, or creating your own budget based on your financial situation.

Having unrealistic financial goals

It’s important to be realistic when setting financial goals, as this will help you stay on track and make progress towards your targets. Some people set unrealistic financial goals because they do not have a clear understanding of their current financial situation.

They may think they can save a certain amount of money each month, when their income and expenditure doesn’t allow for this.

It is also important to consider the time frame you’re working with when setting financial goals.

If you want to buy a house in five years’ time, you will need to factor in the current housing market and your expected salary growth.

If your goal is too ambitious, you may end up feeling frustrated and demotivated.

To avoid making this mistake, you would need to sit down and work on creating a realistic budget before setting any financial goals. Look at your current income and expenditure, and factor in any changes you anticipate in the future.

If you are not sure where to start, speak with a financial planner who can help you develop achievable goals based on your unique circumstances.

Not taking out insurance

One of the most common financial mistakes people make is not taking out insurance. This can be a costly mistake, as it can leave you exposed to a variety of risks. It can put you at risk of financial ruin if you experience an unexpected medical emergency or lose your job.

Even if you are healthy and employed, life is unpredictable and anything can happen. Without insurance, you will have to pay all of your medical bills out of pocket, which can be extremely expensive.

Thus, health insurance is one of the most important types of insurance to have, as it can protect you from high medical bills in the event of an accident or illness.

There are also various types of life insurance which can provide financial protection for your loved ones in the event of your death.

It is important to shop around and compare different insurance policies before deciding. Ensure that you understand the coverage and exclusions of each policy before you purchase it.

Not checking your credit score

Your credit score is a representation of your financial health and it’s important to keep track of it. If you are not regularly checking your credit score, you could be missing out on opportunities to improve your financial health.

A good credit score can save your money on interest rates and help you get approved for loans and lines of credit. A bad credit score can cost you thousands of dollars in higher interest rates and fees.

Maybe you think you have good credit and do not need to check it. But even if you have good credit, it is important to keep an eye on your score. Identity theft and errors can happen to anyone, and they can lower your score.

Thus, your credit score is a key factor in determining your financial health and it is important to stay on top of it.

Borrowing money

Borrowing money can be a necessary part of life, but it can also be a financial mistake if not done correctly. When you’re short on cash, it’s tempting to borrow money from friends or family.

Whether it is taking out a loan or using a credit card, borrowing money can quickly get you into debt. If you are considering borrowing money, ask yourself if you really need it. Can you save up and pay for what you need without going into debt? If not, can you borrow from a friend or family member instead of taking out a loan?

You may feel obligated to repay to your friends or family members the debt quickly, even if you cannot afford it. Thus, it is advisable not to borrow money from them.

If you do borrow from some place else, ensure the interest rates. Be sure to only borrow what you can afford to repay.

Not investing in your future

Investing in your future is one of the most important things you can do for yourself and your family. If you want to secure your financial future, you need to start investing now.

Whether it’s not saving enough for retirement or not investing in education or job training, not investing in your future can have long-term consequences.

Without adequate savings, you may be forced to work well into your golden years instead of being able to enjoy a comfortable retirement. And if you don’t invest in education or job training, you could find yourself stuck in a low-paying job with little opportunity for advancement.

Investing in your future can help you achieve financial security, retire comfortably.

Investing in your future does not have to be complicated or expensive. You can start by simply setting aside some money each month into a savings account or retirement fund.

And if you are looking to improve your career prospects, there are many affordable online courses and programs that can help you gain the skills you need to succeed. Do not let the common mistake of failing to invest in your future hold you back from achieving your financial goals.

The key is to begin Investing early, so that you can reach your financial goals.

Not saving for your child’s future

When it comes to financial planning for your family, one of the worst things you can do is neglect to save for your child’s future. Whether you’re saving for college or for their first home, it’s important to start early and contribute regularly to ensure that you’re giving them the best possible chance at a bright future.

A lot of parents think that they will be able to support their children financially through their own earnings and savings, but this is often not the case.

It’s never too early to start saving for your child’s future, and the sooner you start, the more time their money has to grow. Even if you can only afford to contribute a small amount each month, it will add up over time.

There are a number of ways to save for your child’s future, but one of the most popular is through a 529 Plan. A 529 Plan is a tax-advantaged savings plan that can be used to cover qualified education expenses, such as tuition and fees, room and board, books and supplies, and more.

In every country, the government provides financial plans that support the children and help parents to plan for their children’s future.

If you don’t start saving for your child’s future early on, they may have to rely on student loans to pay for college. Student loans can be difficult to repay and can cause a lot of financial stress.

Conclusion

Financial mistakes can quickly derail your financial goals and put you in an unsuccessful financial situation. Knowing what these common mistakes are and how to avoid them will go a long way towards keeping your finances on track.

Taking control of your finances is key to achieving a secure financial future. Make it easier on yourself by establishing sound habits like budgeting and saving regularly so that you do not get into a difficult situation down the line.

Taking the time now to plan out how you want your money to work for you in the future will pay dividends down the line